The Hyperscaler Comedy Circuit

The market decides whether it wants to laugh, leave, or start arguing about the tab.

THE SETUP — Issue 001

The Hyperscaler Comedy Circuit

The setup always lands. The punchline is negotiable.

Good comedy duos have a clean division of labor. One builds the world, the other blows it up. Abbott sets the table; Costello flips it. Every earnings season, the hyperscalers walk onstage first and tell the market how much money they intend to pour into AI infrastructure. Alphabet says the checkbook is still open. Microsoft talks capacity. Meta raises the ceiling. Amazon keeps building. Oracle occasionally enters like a man who found the side door and would prefer not to explain how.

The market hears all of this before Nvidia reports. That is the key. Nvidia is not just another beneficiary of AI capex; it is the cleanest liquid proxy for the spend. When hyperscalers guide capital expenditure higher, investors do not need Jensen Huang to explain the supply chain. They already know where a meaningful share of that money is headed. The setup begins weeks before Nvidia's earnings call.

That creates a familiar pattern. Hyperscalers report first, capex expectations move higher, and NVDA starts pricing in the confirmation. By the time Nvidia reports, the market has often already bought the story. Then the company delivers the numbers, sometimes spectacularly, and the stock sells off anyway. The joke landed before the punchline arrived.

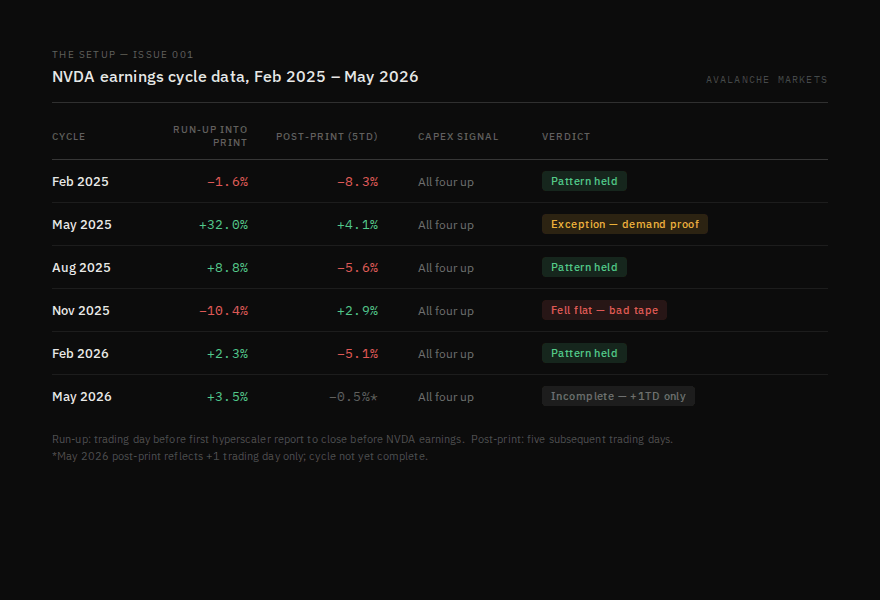

The last six Nvidia earnings cycles show the pattern clearly enough to take seriously, but not so cleanly that it should be traded blindly.

Run-up measured from the trading day before the first hyperscaler report to the close before NVDA earnings. Post-print measured over the subsequent five trading days.

In February 2025, August 2025, and February 2026, the stock followed the classic rhythm: hyperscaler capex strengthened, NVDA rose into the print, and the stock gave back ground after earnings. The signal worked. The exit mattered.

May 2025 was the major exception. NVDA did not just run into earnings; it kept running after the report. That was not a normal confirmation cycle. The market was still litigating DeepSeek and the idea that more efficient AI models might reduce the need for Nvidia's chips. Nvidia answered with $44.1 billion in quarterly revenue, 69% year-over-year growth, and data center revenue up 73%. More importantly, Blackwell demand looked real. The report did not merely confirm the rumor; it weakened the bear case that had been sitting on top of the stock.

November 2025 failed for the opposite reason. The hyperscaler signal was there. Capex was still pointing up. Nvidia beat expectations. In a cleaner tape, that should have supported the stock into the print. Instead, the market was busy arguing about valuation, Fed policy, AI crowding, and whether the data center buildout could earn an acceptable return. The capex signal fired, but the market had changed the question.

That is the real discriminator. Capex direction alone is not enough. The better question is what the market is asking when the capex arrives. In normal cycles, the market asks whether AI infrastructure spending is still real. When the answer is yes, NVDA tends to benefit before earnings and become vulnerable after confirmation. In demand-proof cycles, the market asks whether Nvidia's role in the buildout is still structurally intact. If the company answers that forcefully, the post-earnings selloff can fail. In bad-tape cycles, the market stops asking about Nvidia altogether and starts marking down the entire AI complex.

The trade, then, is not simply "buy NVDA before earnings." That is too blunt, and blunt tools are how traders turn good patterns into expensive lessons. The cleaner version is this: buy the hyperscaler confirmation window when the market is still rewarding AI duration, then respect the risk that Nvidia's actual report becomes the exit, not the catalyst.

Before each cycle, and just like professional comedians, the job is to read the room. If macro conditions are stable, rates are not pressuring long-duration growth, and the market is still paying for AI infrastructure visibility, the setup has room to work. If the tape is already fighting a valuation debate or an AI bubble narrative, the same capex headlines may not carry the same weight. The spending can be real and the trade can still fail.

That is what makes the pattern useful. It is not a law. It is a setup. The hyperscalers write the premise. Nvidia delivers the line. The market decides whether it wants to laugh, leave, or start arguing about the tab.

Avalanche Markets — The Setup | Issue 001

Jason Bartlett

Jason Bartlett is CEO and President of Veche, Inc, parent company to Avalanche Markets. He works extensively in U.S. energy market finance and economics and is a member of the board of Thinking About Thinking, Inc--a 501c3 research and convening organization dedicated to advancing ideas about intelligence.