The AI Infrastructure Trade: Core Thesis Explained

A mania needs belief and egos. This needs concrete and copper.

The numbers have gotten too large to feel real. At some point, a billion became a rounding error. Then ten billion became a product cycle. Now the largest technology companies in the world are discussing capital expenditures in the hundreds of billions, and the market is supposed to nod politely, update its spreadsheet, and move on.

We should probably pause.

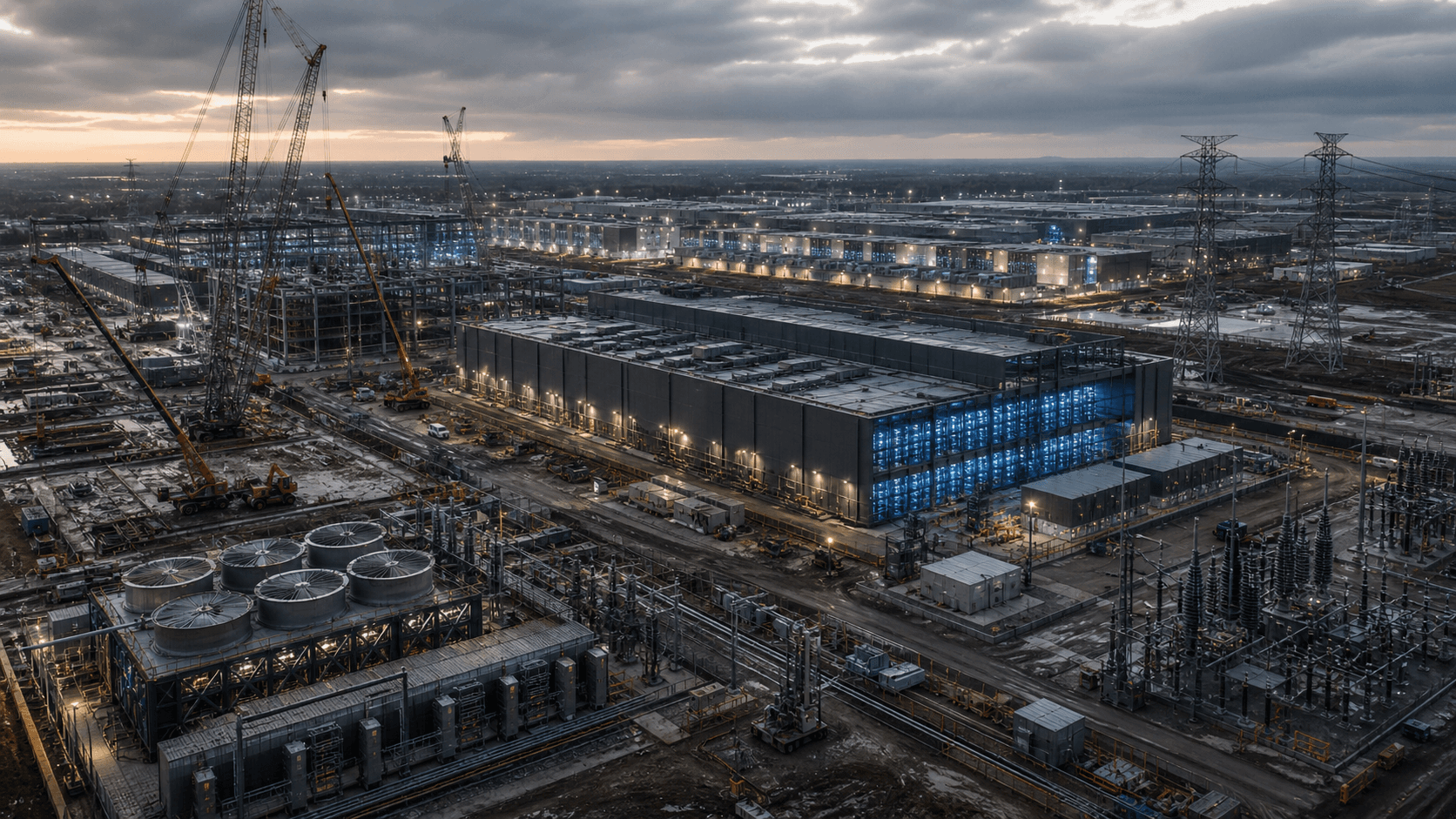

Amazon, Microsoft, Google, Meta, and Oracle are now expected to spend roughly $750 billion in capital expenditures in 2026 alone. That is not a software budget. That is not “innovation spend.” That is not a few engineers in Patagonia vests discovering synergy in a conference room. That is infrastructure.

Steel, concrete, land, fiber, copper, transformers, cooling systems, power contracts, construction crews, GPUs, substations, and data centers large enough to make a Bond villain feel undercapitalized.

This is the AI trade. Not the chatbot trade. Not the “my toaster has a large language model now” trade. The real one. The trade is the physical buildout underneath the entire AI economy.

And the most important thing to understand is this: It isn’t going away anytime soon.

This Is Not a Theme Trade

Nothing ground breaking here, but markets love themes. Metaverse. Cannabis. SPACs. 3D printing. Pick your favorite former revolution. Theme trades are fun because they come with stories. They give investors a clean narrative, a few public winners, and the intoxicating feeling that this time, yes, we are early. Then sentiment turns, the capital dries up, and everyone suddenly remembers what free cash flow is.

The AI infrastructure trade is different. Despite what the software industry will tell you, it is not running on vibes. It is running on purchase orders, construction timelines, power agreements, chip allocations, and multi-year enterprise demand.

The debate is no longer whether AI is “real.” That debate ended when the largest cloud platforms in the world started re-accelerating at the same time. Azure, AWS, and Google Cloud are not meme stocks. They are the toll roads of enterprise computing. When all three start showing renewed strength, the market is not hallucinating demand. It is repricing it.

The question serious traders need to answer is not whether the trade exists, it’s what kind of trade it is. Because if you misclassify the trade, you will mismanage the position.

This Is Not a Cycle Trade Either

Cycle trades mean-revert. Semiconductors cycle. Housing cycles. Energy cycles. Inventories build, demand softens, margins compress, capacity gets cut, and eventually the whole machine resets.

That is not what this looks like. The AI infrastructure buildout is not overshooting some normal level of compute demand. There is no “normal” level to return to. The capacity being built did not previously exist at this scale.

A cycle trade asks, “When does this cool off?” A secular trade asks, “What does this become next?”

This is not a temporary surge in spending. It is the physical construction of a new economic layer. That sounds grandiose, but unfortunately the numbers are grandiose. There is no elegant way to describe trillions of dollars in planned infrastructure spend without occasionally sounding like you are narrating the trailer for a Christopher Nolan movie–”In a world where the entirety of all corporate earnings were dedicated to massive, secular growth…”

Still, the point is simple: The hyperscalers are not renting a bigger office. They are building the railroad. They’re building the internet. Hell, they’re building the next era of humanity.

What They Are Really Buying

The common explanation is that Microsoft, Amazon, Google, Meta, and Oracle are building data centers to meet AI demand. That is true, but incomplete. They are not just building to meet demand. They are building to control supply. That is the center of the entire trade.

Compute is becoming strategic territory. Whoever controls the most efficient infrastructure gets priority access to chips, faster model training, better enterprise relationships, lower unit costs, and more pricing power. Those advantages compound, and once they compound, they become very hard to reverse.

This is why the spending race has become self-reinforcing. The risk is no longer simply “we spent too much.” The greater risk is “we spent too little, and now we cannot catch up.”

That is a very different kind of capital allocation decision. Traditional capex discipline says: slow down when returns are uncertain. AI infrastructure says: slow down and you may permanently lose position. That is why this does not behave like a normal investment cycle.

The companies involved are not making quarterly decisions in the usual sense. They are buying strategic permanence. The companies involved are using today’s cash cows — search, cloud, advertising, enterprise software — to purchase tomorrow’s choke points. None of them wants to be the company that looked at the next platform shift and chose prudence. History is not kind to that guy.

The Market Is Already Confirming It

If this were only a narrative, it would show up in headlines. Instead, it is showing up in relative strength.

Across the AlphaApes universe of more than 3,600 U.S. stocks, leadership is concentrated in the industries that should benefit directly from AI infrastructure spending: semiconductors, electronic components, semiconductor equipment, and engineering and construction..

That is not random. That is the supply chain.

The market is not just buying “AI.” It is buying the physical anatomy of AI: the chips, the parts, the tools, the facilities, and the companies that make the buildout possible.

This is where the trade becomes measurable. A good story can explain why something should happen. A great story is reinforced by the evidence. Leadership is clustering. When multiple companies from the same industry group rise to the top of a 3,600-stock universe at the same time, that is not coincidence. That is institutional money expressing a thesis. That thesis is clear: the first phase of the AI trade is not about the applications. It's the buildout.

The Human Version

Strip away the acronyms and the earnings calls, and the story is almost primitive. A handful of giants have looked at the future and decided they cannot afford to be second. So they are buying land, chips, power, cooling, construction capacity, and time. They are doing it at a scale that makes prior technology cycles look modest.

This is the part that gets missed when the discussion stays trapped inside analyst models. The AI infrastructure trade is not merely a spreadsheet argument. It is a race for control over the substrate of the next economy.

That does not mean every stock attached to the theme goes up forever. It does not mean valuation no longer matters. It does not mean there will be no corrections, shakeouts, or violent reversals, or no moments when everyone suddenly pretends they were skeptical the whole time. There will be plenty of those. Markets are still markets. They exist primarily to humble people with spreadsheets and strong opinions.

But the underlying force is real. Capitalism has been committed. The projects are underway. The supply chain is responding. The earnings are beginning to show up.

That is what separates a powerful secular trade from a speculative mania. A mania needs belief and egos. This needs concrete and copper.

What Could Break It

The thesis is strong, but it is not sacred. Three things need to keep holding.

First, hyperscaler capex has to remain elevated. If the major platforms begin guiding down infrastructure spend, the market will notice immediately.

Second, the supply chain has to convert that spending into earnings. Revenue is nice. Backlog is nice. But earnings leverage is what sustains leadership.

Third, monetization has to keep appearing. At some point, the market needs evidence that this infrastructure is producing durable revenue growth, not just bigger depreciation schedules wearing a futuristic hat.

So far, the signals are holding. Cloud growth is re-accelerating. Infrastructure spending remains aggressive. Supply chain leadership is broadening beyond the obvious semiconductor names and into components, equipment, construction, and power-adjacent businesses.

That broadening is the key. It suggests the trade is maturing, not ending.

The Trade

The AI infrastructure trade is not a bet that artificial intelligence might someday become useful. It is a bet that the most powerful companies in the world have already decided it is useful enough to spend trillions building its foundation.

That decision is now moving through the market: first into chips, then equipment, then components, then construction, then power, and eventually into software, services, and applications. It took over 100 years from the discovery of electricity before the toaster was invented. Nobody got rich off of toasters.

The trade will not move in a straight line. Nothing worth owning ever does. But the direction of travel is clear. This is not a theme exhausting itself. It is infrastructure being built. And once the railroad is under construction, the interesting question is not whether the tracks are real. It is where they go next.

Jason Bartlett

Jason Bartlett is CEO and President of Veche, Inc, parent company to Avalanche Markets. He works extensively in U.S. energy market finance and economics and is a member of the board of Thinking About Thinking, Inc--a 501c3 research and convening organization dedicated to advancing ideas about intelligence.